Objective

By using P-Splines (Penalized Smoothing Splines) to draw a smooth line on two dimensional scatter plot on R.

Code Examples

Sample code from Package ‘pspline’

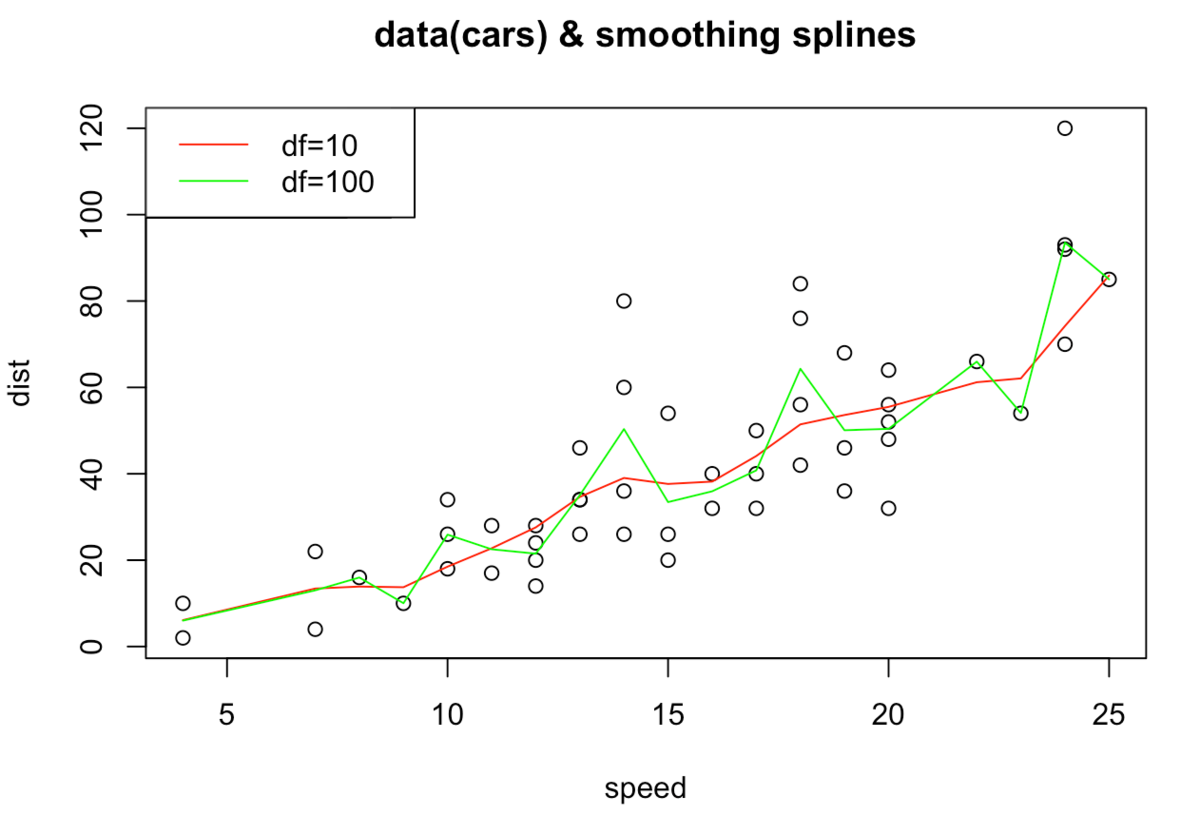

data(cars)

attach(cars)

plot(speed, dist, main = "data(cars) & smoothing splines") # scatter plot the original data

lines(sm.spline(speed, dist, df=10), lty=1, col = "red", ) # draw the P-Spline curve with degree of freedom 10

lines(sm.spline(speed, dist, df=100), lty=1, col = "green") # draw the P-Spline curve with degree fo freedom 100

legend("topleft", legend = c('df=10', 'df=100'), col = c("red", "green"), lty=c(1, 1))

We confirm that the larger df (=degree of freedom) leads to more zigzagged line (bias-variance tradeoff).

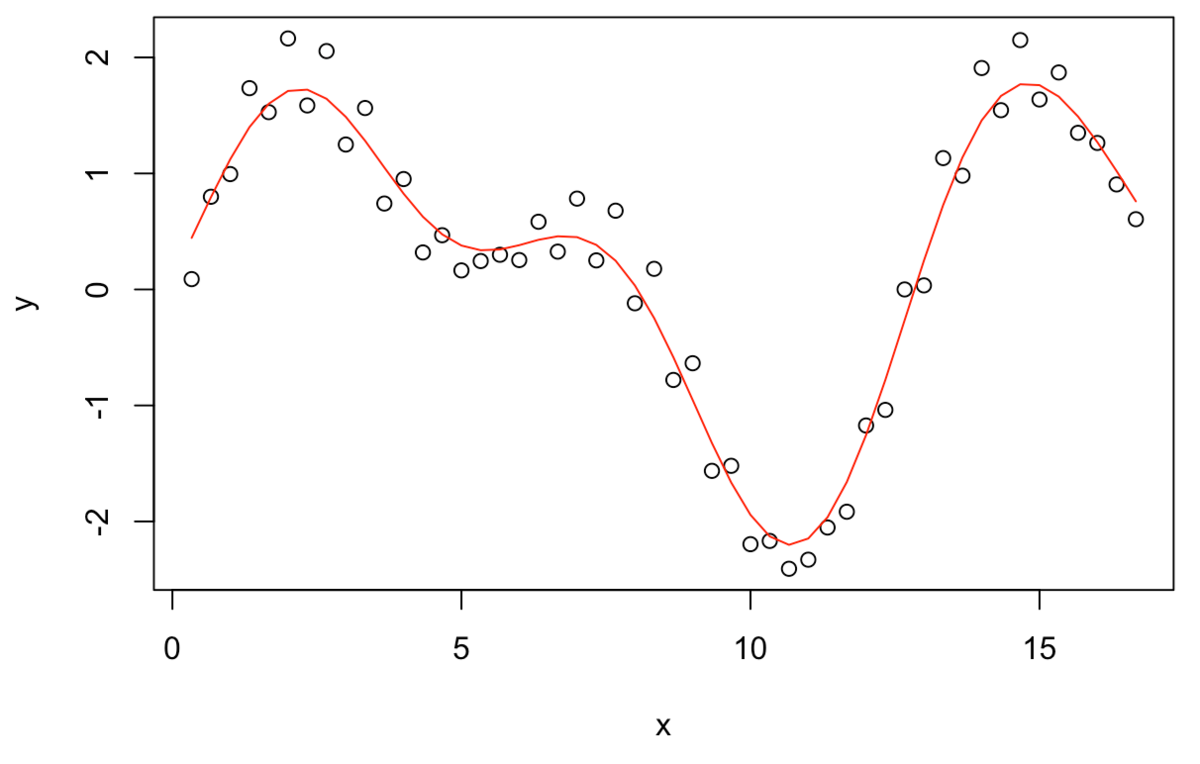

Artificial Data

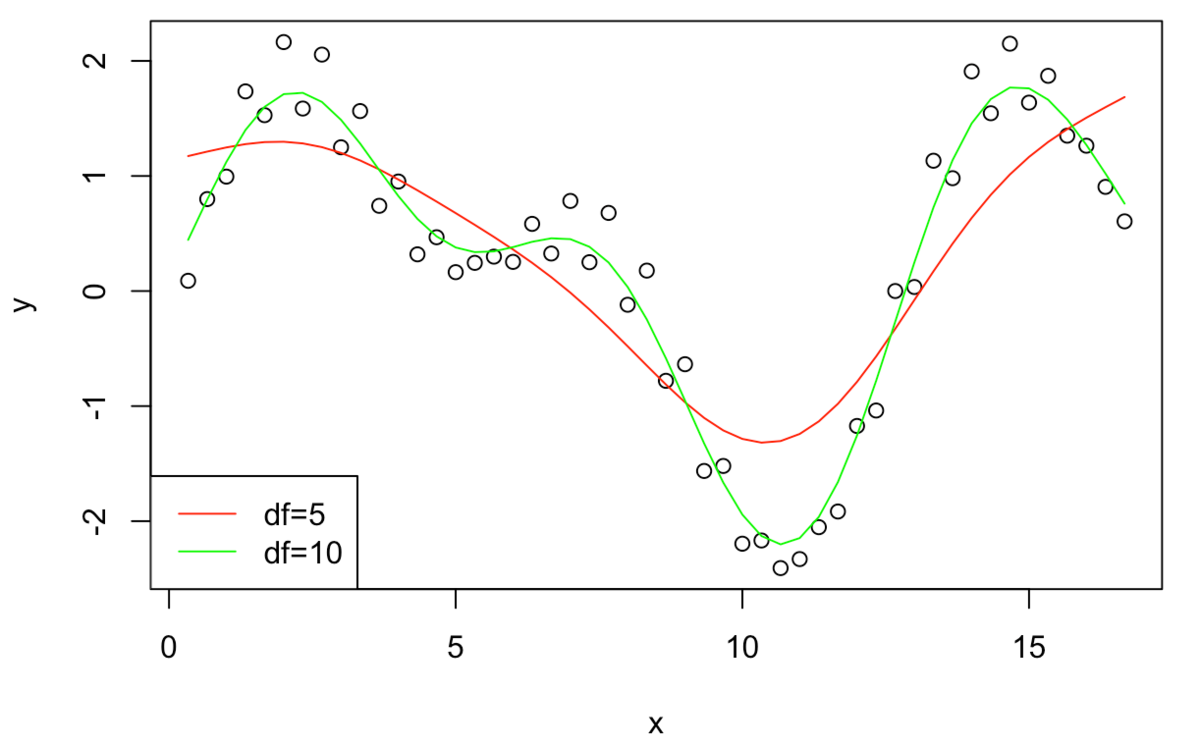

x = (1:50)/3

y = sin(x) - cos(x/2 - 5)*1.5 + 0.3*sin(x*10)

plot(x, y)

lines(sm.spline(x, y, df=5), lty=1, col = "red")

lines(sm.spline(x, y, df=10), lty=1, col = "green")

legend("bottomleft", legend = c('df=5', 'df=10'), col = c("red", "green"), lty=c(1, 1))

Application on Real Data

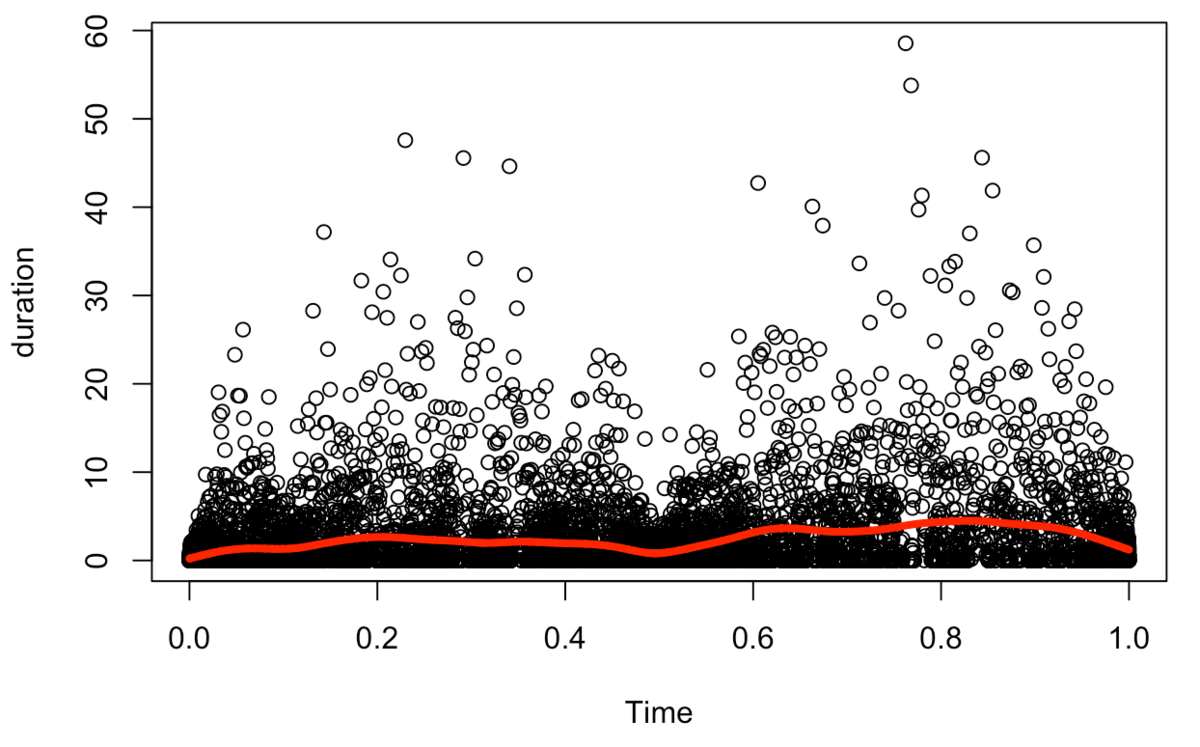

For example, we can apply P-Spline on stock transaction data to extract intraday seasonality

X-axis: time stamps transaction occurred.

Y-axis: trade interval from the last trade

We can confirm the intraday seasonality with P-Spline (shorter transaction interval right after market opens, and right before market closes.)

Mathematical Background

Now, consider

Here, \(x\left(t _ j \right)\) is the spline’s prediction, \(y _ j\) are the actual observed points.

Now, how we decide \(x\left(t _ j \right)\) ?

The first method comes to our mind is probably least square method.

P-Spline utilizes this idea of least square method.

Now, we consider what kind of line we want to draw.

If we have these ↑ points, the line we want to draw would look like this↓

We can also draw a line like this:

But this↑ is not what we wanted. We penalize this zigzag in the P-Spline.

But this↑ is not what we wanted. We penalize this zigzag in the P-Spline.

We define penalty as: